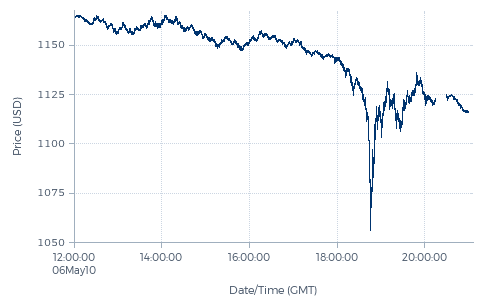

But as it turns out, this approach – even if executed well – is not always profitable. For example, in the Silver flash crash in July, our Diversified Trend Program (DTP) was one of the largest buyers, all the way down to the bottom. Regretfully, the exchange felt it necessary to adjust all prices traded in the flash crash upwards, effectively enabling everyone who sold in the crash to make a profit, irrespective of the disruptive manner in which they executed their orders. Although we do acknowledge that the exchange has the legal right to intervene in such manner, we firmly expressed our disagreement and concern. We strongly believe that such intervention undermines the proper functioning and fairness of the market.

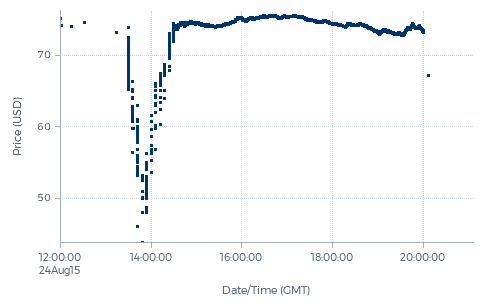

The flash crash-type volatility, however, is not the type of volatility we are specifically aiming to capture with our investment programs. But since these flash crashes do happen regularly, it is essential to ensure that we do not contribute to them and that we do not lose money because of them. Our execution strategies are designed to prevent that from happening. And as a bonus, we regularly are even able to profit from short-lived spikes and flash crashes.

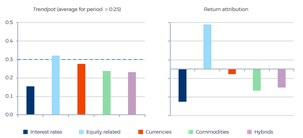

What is the type of volatility we are really after? The market volatility shaped as trends. In other words, a significant price move from one price level to another – either higher or lower – that takes some time to complete. At least a few weeks, but preferably somewhat longer. Some call this directional volatility. Such volatility is not measured by the traditional volatility measures, but is effectively captured by our trendpot measure, which we introduced in 2010. Trends such as defined above result in a high trendpot figure. And by the way, the hypothetical zero-volatility 0.1% daily price rise or fall mentioned earlier would do so as well. Spikes and flash crashes, on the other hand, typically do not impact trendpot.