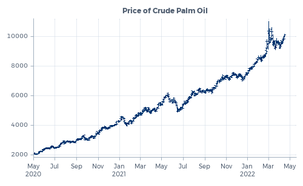

Part of these supply chain issues were related to the covid pandemic. Everyone will have heard about the global chip shortage. Some of the world’s largest semiconductor factories in Asia were shut down early in the pandemic for up to a few months. Meanwhile, some demand for chips temporarily fell away, but people working from home created more demand for hardware that requires chips. So far, producers have not been able to catch up with demand. Covid also caused logistic problems. As a legacy from the Asian lockdown, western harbors are now filled with empty containers that should be in Asia for an efficient shipment of goods out of there. And travel restrictions caused problems in the labor market. Malaysian palm plantations are still dealing with a shortage of foreign workers to pick the fruits from their trees. This is one of the reasons why the price of palm oil has increased fivefold since April 2020.

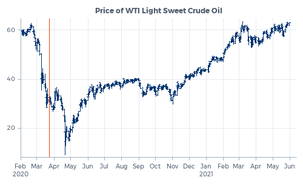

Another part was weather related. In the summer of 2021, the temperatures in British Columbia climbed to 50 degrees Celsius. Without refreshing showers, that is absolutely not why canola once decided to start growing there. In other regions in the world, heat and drought harmed other crops. For instance in New Mexico. Chile peppers may be the hottest commodity, but they don’t do well above 95 degrees Fahrenheit. In July 2021, the temperature peaked above 100. That same month, many European farmers weren’t able to harvest a decent quality wheat crop due to heavy rains and floodings. And that same summer, rain shortage threatened the production of hydropower in Norway and shortage of wind above the North Sea reduced production of wind energy. These were only two of the factors contributing to a European energy crisis. European/Russian geopolitical tensions added to that.

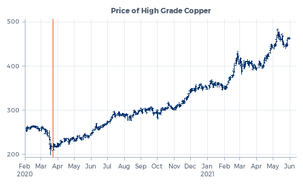

The extreme weather conditions that caused these problems seem to have been manifestations of the ongoing climate change. For countries to reach their emission reduction targets, among others an energy transition away from fossil fuels to renewable sources is required. This development has made our economies more vulnerable to production issues relating to for instance wind and hydropower. And this transition is also increasing demand for metals like copper, nickel, aluminum and cobalt. A complicating factor is that the production process of for instance aluminum itself is highly polluting. Climate change is therefore a huge challenge for commodity markets — both combatting it and not combatting it causes supply chain issues.

The most recent factor adding to these supply chain issues has been the Russian invasion of Ukraine. Both countries are major producers and exporters of a wide range of commodities, including energies, metals and grains. The war itself has a direct impact on the production in, and export from Ukraine. The various implemented and threatened sanctions from both sides — imposed by the importing countries as well as by Russia — further limit the supply of many commodities. This for instance includes fertilizer, which could negatively impact the production of crops, also those far away from the battlefield.