Recent developments in the cocoa market received some media attention discussing the impact of computerized trading. In this article we provide some color on the cocoa market and the role and responsibility of investors in this market.

May 2018 ●

9 min read

Harold de Boer

Managing Director / Head of R&D

Share

There are grounds for questioning whether commodity futures markets continue to fulfill their fundamental role in the price discovery process.

Computerization is a fact of life. As are some other global developments. Not all markets have already fully adapted to this change.

Well-functioning markets require responsible investors who are conscious of their role and their impact.

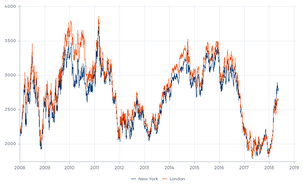

Among the strongest rising commodities so far in 2018 is cocoa. In New York the nearby futures contract has risen more than 50 percent in four months’ time. A recent Financial Times article’s headline identified the cause: “Computerised trading drives up New York cocoa price”. ⁱ Computers were behind not only the price rise, but also a “dramatic divergence in the longstanding price relationship with the London market.”

The article discusses “waves of buying and selling by speculative funds, many believed to be driven by algorithms”. It cites brokers stating that “anonymous computerised strategies now dominate flows in the New York market.” And that the market is “in the grip of technical, system-led buying.” It then gives the floor to the renowned commodities trader Anthony Ward, who closed his fund at the end of 2017, exiting the cocoa market. Mr. Ward blames “the rising power of algorithmic and systems-based trading for making position-taking based on fundamental supply and demand factors more difficult.”

Graph 1 – Price of New York and London cocoa futures in $ per metric ton

The basic concern is that the price development in the cocoa futures market does not match the developments in the underlying physical market. As such, the futures market seems to falter in fulfilling its fundamental role in the price discovery process.

We share that concern. In the past decade we have noticed reoccurring signs of such disconnection in a host of markets, including various agricultural commodities. We attribute this to evolving technologies and to the changing mélange of market participants: the entrance of new players with different aims and strategies, the departure of traditionally dominant players, and to existing players that did not yet adjust their way of operating to this changing environment. Transtrend itself has been an active participant committed to this changing market since the early ‘90s. We, meaning the market as a whole, do not seem to have found a new robust and sustainable symbiosis yet.

But as much as we share the concern, we do not think that simply blaming computerized trading is a step towards a solution. As it is, computerized trading is a rather meaningless term anyway. Nowadays, in New York as well as in London, cocoa futures are traded only on electronic trading platforms. These are only accessible by computer, which in essence makes all cocoa futures trading computerized. Critics using the term computerized trading will typically do so with a reference to the nature of the process that leads to the decision to buy or sell. But whether or not a computer is used in that process is not really relevant either. A human trader could closely watch the cocoa prices in New York and London, and decide to place an order to sell in New York and to buy in London when he observes a significant price difference. But he could also program his computer to do the exact same thing. From a market impact point of view, that does not make any difference. Especially not when he uses the same algorithm to execute these orders.

The cocoa futures market seems to falter in fulfilling its fundamental role in the price discovery process.

In our March 2018 market report we wrote: “Unfavorable weather in Ghana drove the price of cocoa up." Technically, that was not necessarily true. Basically, the only force that drives market prices is the aggregated market impact created by all market participants. The price of cocoa rises only because buyers are bidding a higher price than they did before and/or sellers are asking a higher price. Whether they do so because of drought in the western African growing region is something we can only guess. But effectively, that doesn’t matter. For a market to function well, the only requirement is that when shortages loom, the futures price rises in time to give producers an incentive to raise their production, or to give consumers an incentive to find alternatives. And again, it is irrelevant whether or not these buyers and sellers are aided by software at any point in their decision-making and communication process.

A more meaningful distinction is whether or not the decision to trade cocoa futures is made ‘with an eye on the cocoa market’. This holds for instance for commercials who buy futures contracts to hedge their future physical cocoa demand, for instance to produce chocolate cakes. Such commercials will only be willing to pay a higher price when they expect to be able to pass on these higher costs to the buyers of their delicious cakes. And this also holds for speculators who are sufficiently convinced that the cocoa price could rise above the price they bid to take on the price risk associated with the speculative position they will acquire when a seller takes that bid. But that typically does not hold for market participants who buy cocoa futures irrespective of price without a view on the cocoa market.

Among these ‘eyeless’ market participants are the passive investors allocating funds to commodity indices. In our research we have found strong indications that these capital flows have a potentially disturbing market impact. It does not necessarily drive up commodity prices above their reasonable levels. But the ‘blindly’ repetitive process of buying further-ahead futures to sell them as they approach delivery does impact the term structure of futures contracts, resulting in higher costs of hedging for the demand side. Ultimately this results in a higher price to be paid by the chocolate consumers; they pay a premium that the farmers producing the cocoa beans will not receive.

A regularly recurring market-disturbing impact results from major capital flows into or out of commodity indices, when these flows are driven by global market factors that in themselves do not drive the specific commodities. This is especially the case for commodities like cocoa whose supply and demand factors are typically local, such as the climatological conditions in a rather limited growing area. And this is even more so with flows into or out of commodity funds that are not weighted based on production quantities or market liquidity, but instead are ‘risk-balanced’ with a higher allocation to lower-correlated commodities. Such commodity funds are effectively designed to send disturbing price signals to smaller-sized low-correlated markets.

Getting to the cocoa futures price in 2018. Did it rise too high given the crop conditions in western Africa? The producers do not think so. At the World Cocoa Conference 2018 held in April, the Cameroonian trade minister Luc Magloire Mbarga Alangana declared in his speech that the prices are still very low. “The producer countries can no more agree with the actual cocoa prices which sounds like slavery,” he said. Of course, the minister of a cocoa producing country has an audience to serve.

However, note that while a 50 percent price rise may sound like a lot, that does not mean that the resulting price level was at all remarkable. Due to a tumble of more than 40 percent in the cocoa price in the preceding two years, it is just a recovery from a worrisomely low level. Those low prices had seriously harmed the growers. Many of them saw no other alternative than to cut spending on their farm maintenance. And this lack of investment on their part had made the cocoa yields more vulnerable to the hot and dry weather in early 2018. It does not take a computer to understand that this market required a price rise. But those market participants who did use a computer are not necessarily out of their minds if they reached the same conclusion.

What about the “dramatic divergence in the longstanding price relationship with the London market”? To attribute this to computerized trading is even stranger. London may be located on an island, but for the “anonymous computerised strategies” the London cocoa futures platforms are just as accessible as the New York platforms. One of the undisputed virtues of electronic trading platforms with global access is that unfounded dislocations in futures prices can easily be arbitraged away. But that of course does not apply to substantiated price differences.

Graph 2 – Price difference between New York and London cocoa futures in $ per metric ton

By March 2018 the warehouses in London were packed with bulk bags of low-quality cocoa beans from Cameroon. These bags were certified for delivery on the May futures contract. But since the quality of these beans was not going to improve with age, traders doubted whether this cocoa would get recertified for delivery on the July contract. And they surely did not expect to be allowed to deliver these bags on the higher priced futures contracts in New York. So traders taking delivery on the May contract in London were well aware that they ran the risk of getting stuck with a bulk of low-quality cocoa beans. Again, it does not take a computer to understand that this quality issue drove the prices in London below the prices in New York. As it also drove the price of the May contract in London below the price of the contracts further ahead.

Graph 3 – Price discount of May vs. further away London cocoa futures contracts in $ per metric ton

Of course, we cannot prove whether a market is priced right. No one can, since there will never be unanimity on this. Even in a perfectly functioning market there will always be some participants who think the price is too low; these are the ones bidding at that price. And there will be others who think the price is too high; these are the ones offering. A robust equilibrium requires the opposing forces driven by these different views. Disturbing a market requires market impact that is not founded on a view on that particular market.

Studying the recent developments in the cocoa market, we find no grounds to support the argument that computerized trading has driven up cocoa prices above reasonable levels. Nor do we support the statement that computerized trading has sparked an unreasonable divergence between the prices in New York and London. But we also would not claim that the recent functioning of these markets is perfect. Financial markets in general have undergone fundamental changes in the past decade. And especially some commodity markets that typically should be driven by local factors seem to have a hard time to fully adapt to the threats and opportunities that came along with a changing world.

Studying the recent developments in the cocoa market, we find no grounds to support the argument that computerized trading has driven up cocoa prices above reasonable levels.

The entrance of new players with different aims and strategies does impact any market. As does the departure of traditionally dominant players. The Financial Times article gives a perfect example of this. It states that commodities trader Anthony Ward was dubbed “Chocfinger” due to his influence over the cocoa price. In case of a large price difference, he would buy physical cocoa in London and send it to New York. If this trader indeed had such influence over the cocoa price during his active years, it would be strange if his exit did not impact the market. The departure of a dominant player does change the playing field. In the short term, that can lead to disturbances. A healthy market will adapt for that.

A market like cocoa is, among other things due to its limited major growing region, more vulnerable to disturbances than most other markets. Like any other market, the functioning of this market requires an interplay of producers and consumers, of shippers and warehouses, of commercials and speculators, of risk avoiders and risk takers, of short-term players and long-term participants. But more than for most other markets, the well-functioning of a market like cocoa requires all these participants to be aware of their role and their impact. And this responsibility includes adapting to a changing world with high-speed communication and computer terminals in buildings that historically would have been crowded with humans.

Source of price data used in the graphs in this article: Thomson Reuters, Bloomberg and Transtrend.

ⁱ Emiko Terazono, “Computerised trading drives up New York cocoa price”, Financial Times, 26 April 2018.

We use cookies to ensure that you enjoy the best experience on our website. We do not use any third party cookies.

Our website may, however, include hyperlinks to external websites that use third party cookies.

For further information, please read our

Privacy statement

and

Terms of use.