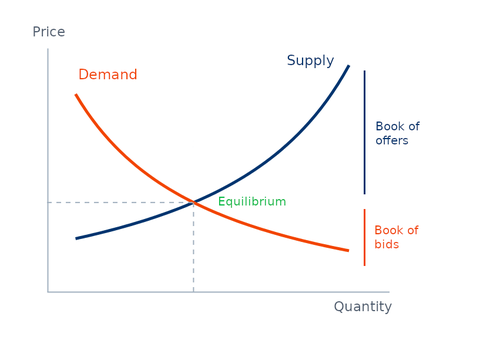

According to traditional equilibrium theory, additional buyers entering the market will cause prices to rise. To get their orders filled, buyers will have to bid up the market to replace less aggressive buyers and/or to meet the demand of the less aggressive sellers. This price impact is part of the transaction costs of an investment strategy. The academic community used to give considerable attention to these costs in their research and papers.

An example related to our business is a research paper on the profitability of technical trading systems conducted by Lukac and Brorsen in the late ‘80s, published in The Financial Review in November 1990. In their testing the authors assumed transaction costs of $100 per contract. In the presentation of their results they noted: “Results were quite sensitive to assumptions about transactions costs due to the relatively small returns per contract traded.” These kinds of remarks were quintessential for the academic finance literature in the ‘80s, which was often aimed at testing the Efficient Market Hypothesis in some form. Common practice was that articles showing evidence of non-efficiency were questioned on their assumptions around transaction costs. Would their conclusions still hold if ‘more realistic’ assumptions were made?

In contrast, in a comparable piece of research conducted by Hurst, Ooi and Pedersen, published in the Journal of Investment Management in February 2013, the authors stated: “The strategy returns are gross of transaction costs, but we note that the instruments we consider are among the most liquid in the world.” The fact that this article has been accepted for publication in a peer-reviewed community illustrates a remarkable development in academic practice. Apparently, the idea that trades can be executed without market impact has become generally accepted – a 180-degree turn in culture compared to three decades ago.

What academia nowadays teaches or publishes is put into practice by the students of this new version of microeconomics. A result of that is the May 2010 flash crash in the S&P 500 futures, indisputably one of the most liquid instruments in the world. According to an SEC/CFTC report, this crash was triggered and fueled by a large mutual fund that “sold a total of 75,000 E-Mini S&P contracts (valued at approximately $4.1 billion) without regard to price or time” – another example of price-insensitive execution. According to traditional economics, a market would indeed not be functioning properly if such a large sell order would not cause a price decline. Prophets of the new school of economics, however, have come up with various alternative explanations for this flash crash.

But if execution has no market impact anymore, what other force would then make markets move? It is still generally accepted that Apple’s stock price should rise when Apple is very successful in developing, producing and selling its products. But how should that price rise materialize when it is not due to the market impact of investors buying the stock? Should the correct price level be set by a central committee like the former Soviet fondoderzhateli? Or should the correct price be determined by the market supervision department of the exchange? If so, this would turn the exchange into a shop.